MuniFin’s net operating profit excluding unrealised fair value changes amounted to EUR 74 million in the first half of the year. A year before the figure was a record-high EUR 108 million. This year’s drop was expected, as it was influenced by the change in credit terms applied in late 2021.

New lending in January–June amounted to approximately EUR 2 billion and the long-term customer financing excluding fair value changes grew by 2.6% and totalled EUR 29.8 billion.

The amount of green finance aimed at environmentally sustainable investments totalled EUR 2,700 million (EUR 2,328 million) and the amount of social finance aimed at investments promoting equality and communality EUR 1,296 million (EUR 1,161 million) at the end of June.

In January–June, new long-term funding reached EUR 5,962 million (EUR 6,025 million). Group’s consolidated statement of financial position grew to EUR 47.5 billion.

– The pandemic has transformed our lives into something that is predicted to become the new normal, but the outlook has become even murkier than expected after the war broke out in Europe. Amidst all this uncertainty, it is important to note that at MuniFin, we work hard every day to create stability in these uncertain times and to ensure smooth operations for all our customers, notes Esa Kallio, President and CEO at MuniFin.

At the end of June, the MuniFin’s capital ratio was very strong. The Group will also publish a separate Pillar III Report on risk management and capital adequacy on August 8.

The Russian invasion of Ukraine has fundamentally changed the outlook of the Finnish economy. Not only has consumer confidence weakened, but the business expectations have also taken a slight downward turn. Despite the challenging outlook, the Finnish economy is facing the future from a better position than it did when the COVID pandemic hit, and the future NATO membership should help to clarify Finland’s security position.

Rising costs and interest rates are overshadowing the economy and the construction sector in particular. In general, the operating environment is now far from optimal for investments. Finland’s future NATO membership should help to clarify Finland’s security position and strengthen confidence in Finland as a safe target for investments in the long run.

Weakening purchasing power poses the greatest risk

Despite the challenging outlook, the Finnish economy is facing the future from a better position than it did when the COVID pandemic hit.

The service sector has revitalised after restrictions were lifted, and many industries still have strong orderbooks so industrial production is expected to keep growing at least for the rest of the year. The growing trend in employment has continued despite the war in Ukraine, and the employment rate has already risen to around 74%. The seasonally adjusted unemployment rate has fallen close to 6% and is now at its lowest level since 2008.

The biggest uncertainty factor in domestic economy is the accelerating inflation and its effect on domestic consumer demand. In January–March, the real income of full-time employees decreased by 2.7% from the previous year. Such a drop in real income has not been seen in Finland since the late 1970s.

To some extent, consumer price inflation is driven by a change in relative prices, to which households can adjust by changing their consumption habits, but the majority of the cost pressure comes from rising prices of necessities, such as food, fuel and housing. Debtors’ interest expenses are also on a rise. Some households have additional pandemic savings, which may mitigate the effects of their declining purchasing power to some extent.

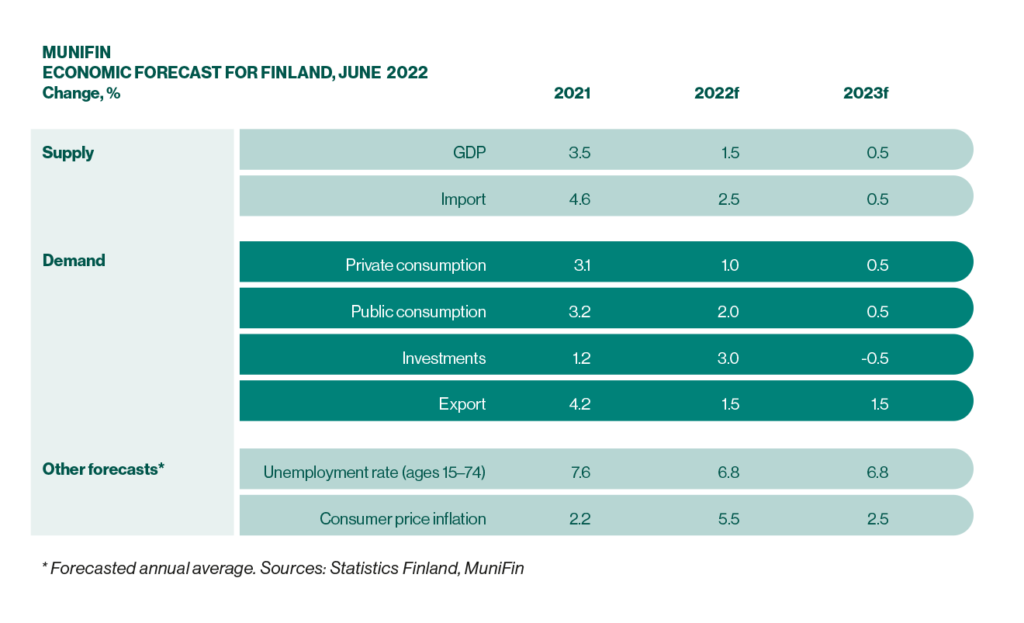

GDP will grow moderately in 2022, but 2023 is looking highly uncertain

The Finnish economy is relatively strong, but the growth outlook is bound to deteriorate because of the war in Ukraine, the rising inflation and the rapidly tightening monetary policy. The Finnish GDP is expected to grow very little during the rest of the year, and negative quarters are also possible.

Thanks to last year’s strong growth trend, however, the Finnish GDP is expected to reach an overall growth of 1.5% for 2022. The next year, on the other hand, is expected to be more difficult: our current estimate for GDP growth in 2023 stands at 0.5%, and that, too, requires that the economy starts to recover during 2023.

The weakening economic outlook also affects employment growth. The share of hard-to-fill vacancies is higher than during previous cyclical peaks, and talent shortage is so serious a problem that it limits recruitment in itself. Nevertheless, due to the recent sharp decrease in unemployment, we have lowered our estimate of the overall unemployment rate. We now expect it to average around 6.8% for both this year and the next.

It now seems that inflation will not relent until early 2023. We expect Finnish consumer price inflation to stand at 5.5% in 2022 and at 2.5% in 2023.

This summary of MuniFin’s Economic Forecast (only available in Finnish) is written by Timo Vesala, Chief Economist, Doctor of Philosophy (PhD), Economics.

The idea for the culture book was sparked last spring, when it turned out that the different descriptions of MuniFin’s working culture and practices were spread out across different documents. At first, the goal was simply to compile all the relevant documents in one place, but along the way, this work transformed into a culture handbook.

“We invited all MuniFin employees to participate in the work. The culture book is a result of the collaboration of various experts across the organisation”, says Tiina Lammi, Communications and HR Development Specialist at MuniFin.

As the head of company culture development at MuniFin, Lammi has been involved in the creation of the culture book from the start. Through a collaborative process, the MuniFin team distilled the company’s cultural cornerstones into communality and team spirit, transparency and trust, and sustainability and social significance.

“We want these three cornerstones to be our guiding principles in all our work”, Lammi says.

An important role in society brings people together

Lammi started out at MuniFin as an assistant in 2011. Her career path spans more than a decade and exemplifies the kind of employer MuniFin is and strives to be.

“MuniFin has a very strong company spirit. Even though a lot of new people have joined the company during my time here, MuniFin has been able to keep that small business feel. I’m very grateful that I’ve had the chance to take on exciting new roles. We have a real opportunity to shape our job descriptions, and that is extremely valuable for employees”, Lammi commends her employer.

“People here are used to our flat hierarchy, and everyone is easy to approach. Despite our growth in recent years, we are still very much one team and closely involved in cultural work”, notes Jukka Leppänen, Head of Customer Relations at MuniFin.

The single most important factor that unites MuniFin employees is the company’s significant role in society. MuniFin is a small community with a big impact.

“Our work touches the lives of all Finns. We finance hospitals, schools, day-care centres, affordable rental housing, public transport solutions and a whole host of other projects. We help build a more sustainable and equal Finland. For many of us, this is the most important reason for coming to work every morning”, Leppänen explains.

The culture book is by no means the end of MuniFin’s cultural work. In fact, strengthening the company’s culture is a written-down objective for 2022 across different levels of the organisation.

“Of course, hybrid work makes it more challenging for employees everywhere, also at MuniFin, to commit to their organisation and its culture. We are constantly looking for new ways to preserve and bolster our culture together with our employees”, Lammi says.

Leppänen emphasises the importance of inclusion and everyone’s responsibility in culture building.

“Companies can change their strategy and vision quickly, but it takes time to build and shape the company culture. The management alone cannot dictate or define the company culture, but it does have a particularly strong role in creating it.”

On 10 May 2022 MuniFin priced an EUR 500 million fixed-rate green benchmark due 17 May 2029. Utilizing a supportive issuance window and a strong demand for green assets, MuniFin opened books at 8:15 London time with price guidance at mid-swaps –8bs area. The limit was fixed to EUR 500 million.

The demand was strong from the outset and just in two hours the spread was tightened by 3bps. Shortly after, the books were closed in excess of EUR 1.4 billion. The transaction pays a coupon of 1.5% (annual) and a spread of mid-swaps – 11bps.

The transaction attracted a significant amount of ESG investors: nearly 80% of the final orderbook went to green investors. Central banks and official institutions took 38%, Asset managers 24% and bank treasuries 22%. Geographically; Germany, Austria and Switzerland took 24%, followed by BeNeLux at 23% and Nordics at 16%.

“The multiple times oversubscribed transaction shows us, once again, how solid our investor base truly is. Despite the volatile atmosphere in the market, our green bond attracted also brand new investors. We are extremely pleased with the outcome and especially the great support from the ESG investor community”, says Analyst Lari Toppinen from MuniFin funding team.

MuniFin has offered its customers green finance for sustainable investments since 2016. Funding for green projects is sourced by issuing green bonds. For investors, MuniFin’s green bonds offer a way to finance positive impacts through carefully selected projects in e.g. sustainable building, public transportation and renewable energy categories.

1.5% annual, Actual/Actual (ICMA), following unadjusted

Pricing Date:

10th May 2022

Payment Date:

17th May 2022

Maturity Date:

17th May 2029

Mid Swap Spread:

-11bps

Joint Bookrunners:

BNPP, Danske Bank, NatWest, SEB

Comments from bookrunners

“Congratulations to the MuniFin team for successfully launching their second EUR benchmark and first green bond of 2022. To execute such a solid transaction given the volatile market backdrop is a strong testimony of Munifin’s ability to build a strong and diversified investor following.”

Salma Guerich, DCM SSA, BNPP

“Congratulations to MuniFin on their highly impressive return to the EUR Green Bond market. With final pricing through fair value and a large and high quality orderbook in challenging market conditions, this truly demonstrates the strength of the credit and the support that MuniFin enjoys from the ESG focused investor community. Danske Bank is proud to have been part in this successful transaction.”

Axel Zetterblom, SSA Origination, Danske Bank

“A fantastic return to the Green Bond market for MuniFin. The quality of the investor base came through from the outset with investors showing strong support for the first MuniFin Green issuance of 2022. Amidst a more volatile backdrop, the extremely positive reception exemplifies the quality and demand for the MuniFin name, and support for their Green framework. We are very proud to have been involved at NatWest,”

Kerr Finlayson, Head of FBG Syndicate, NatWest

“SEB is delighted to have taken part in MuniFin’s latest triumph in the EUR Green bond market. Despite significant market volatility creating a challenging backdrop, the transaction garnered a high-quality, multiple times subscribed order book, and a final reoffer level through the fair value curve. This is a clear demonstration of MuniFin’s long-standing reputation amongst the ESG investor community.”

Rebekah Bray, Deputy Head of SSA Origination, SEB

Further information

Joakim Holmström – Executive Vice President, Capital Markets and Sustainability

In June 2021, the Finnish Parliament adopted the legislative package on Finland’s health and social services reform. From the beginning of 2023, the responsibility for organising health, social and rescue services will be transferred from the municipalities to the 21 self-governing wellbeing services counties. The City of Helsinki is an exception: it will be responsible for organising these services within its own area.

The wellbeing services counties are responsible for organising public services such as primary healthcare, specialised medical treatment, social welfare, dental care, mental health services, substance abuse treatment, services for the disabled and housing services for the elderly. Municipalities will continue to provide day care, education, and sports and culture services, for example.

The health and social services reform aims to ensure equal and high-quality health and social services, improve their availability and accessibility and curb their increasing costs. The reform also seeks to reduce health and welfare inequalities, secure the availability of skilled employees and meet the challenges created by demographic changes.

The legislative package adopted in June enables MuniFin to continue to act as the financier of loans transferred from municipalities and joint municipal authorities to the new wellbeing services counties. The Finnish Parliament is currently working on amending the Act on the Municipal Guarantee Board, a key piece of legislation for MuniFin’s operations. If implemented, this amendment would allow MuniFin to finance new investments by the wellbeing services counties and the companies and organisations that they control. This amendment is planned to take effect on 1 May.

The Finnish Financial Supervisory Authority (FIN-FSA) has decided that like the central government and municipalities, wellbeing services counties will also fall in the zero-risk category in the capital adequacy regulation of banks. This decision brings the wellbeing services counties on par with municipalities when it comes to the availability and efficiency of funding. The decision is a welcome one, as long-term investments should be made with long-term financing.

The demand for financing in the municipal sector was moderate and lower than expected in 2021. This was due to an unexpectedly good economic and employment situation and the central government’s COVID-19 support for municipalities. In contrast, the demand for non-profit housing finance grew moderately and has remained largely unaffected throughout the pandemic. Our new long-term financing for 2021 totalled EUR 3.7 billion.

What was 2021 like at MuniFin? Watch the video below.

This year, we report the impacts of our green and social finance in separate reports. We grant green finance to projects that have verifiable positive impacts on the environment and social finance to projects that produce widespread social benefits.

Integrating sustainability and new operating models

Sustainability is interwoven even more closely into all our operations and the work of all our employees. In 2021, we started to work on calculations to make the environmental load of our own operations more visible. We also published our Sustainable Investment Framework, which summarises the sustainability principles, processes and responsibilities in our investment activities. Because sustainability is such an integral part of all our work, we have incorporated it directly into our operational reporting for the first time, instead of publishing a separate report.

MuniFin’s year 2021 was characterised by renewal and the rooting of new operating models.

“This year, we will continue to renew, improve our management and integrate sustainability into our operations even more closely”, says Esa Kallio, MuniFin’s president and CEO.

The pace of financial regulation has been accelerating since the late 1980s, with the financial crisis ramping up the speed even more. Developments in regulation have not always been straightforward or even logical, but despite their flaws, they have brought security and stability to our operations, customers and the market.

Tighter capital and liquidity requirements

The COVID-19 pandemic has highlighted the importance of the stability of the financial market. Banks have demonstrated their ability to operate during the crisis, in part thanks to the capital and liquidity buffers imposed on them. The economy as a whole has also not suffered as much as feared.

Harmonisation has made banking requirements clearer in general, but accounting for the specificities of the different business models is a difficult task.

Risk management and reporting

Different ways to identify, address and manage risks have evolved substantially over the years, and the importance of risk management is well understood across banking organisations. However, risk management has become such a multi-faceted and complicated process that it can sometimes be challenging to see the wood for the trees.

Reporting to the authorities has become somewhat of an art form, requiring specific reporting skills in addition to financial administration skills. Reporting currently serves the purposes of the authorities and not the businesses themselves, and as a result, the same data is being reported multiple times in an inefficient way. It would be beneficial to eliminate these overlaps and streamline reporting practices, but looking at the current roadmap of regulatory development, this does not seem very likely.

Requirements for investment services

The provision of investment services involves a considerable amount of reporting and information sharing between authorities, customers and other market participants. The rules are made to provide security for everyone in the market, but they also assist the authorities in their supervisory work to promote market stability.

Information overload can make investment services difficult to approach, but it is not the original purpose of regulation. This problem could perhaps be solved with legal design, which means making regulation and the relevant documentation more user-friendly and understandable.

MuniFin provides investment services on a relatively small scale, but the new regulation has nevertheless affected us substantially – perhaps even more than the regulators intended.

Necessity is often a good motivator. The current operating environment could have come about through independent market developments, but at a slower pace and with much more variation between different organisations.

Faster globalisation is challenging traditional operating models

Globalisation is accelerating and posing major challenges for the traditional approach to regulatory work. Very few things concern only individual countries these days. Time will tell whether regulation based on strict geographical boundaries will become downright impossible.

The European Union has partially tackled this issue by creating an European market. But the euro area and the European Union are not the same thing, which already creates many new regulatory nuances. Global phenomena will not stop at some boundaries drawn on a map; a good example of this is climate change and the EU Taxonomy for Sustainable Economic Activities, which seeks to speed up the achievement of climate goals by linking the funding of investments to their environmental impacts.

In the future, regulation will be problematic not only because of climate risks but also because of cyber threats, as a cyberattack can strike anytime from anywhere in the world. Regulation has the potential to make the world a better and safer place, but this requires more global cooperation.

At MuniFin, we closely monitor regulatory developments that are relevant to our own operations and aim to influence potential problem areas. In this constantly changing world, nobody has all the answers, but through open dialogue and cooperation, we can bring about regulation that truly advances society.

Mari Tyster Executive Vice President, Legal and Communications, Deputy to the CEO, and Member of the Executive Management Team at MuniFin

The Group’s net operating profit excluding unrealised fair value changes amounted EUR 213 million (EUR 197 million) and it increased by 8.0% (6.2%). The Group’s net interest income totalled EUR 280 million (EUR 254 million) and grew by 10.3% (5.8%). Costs in the financial year amounted to EUR 72 million (EUR 58 million). Costs excluding the non-recurring item grew as expected and were EUR 2.6 million higher, making the figure 4.4% greater than in the previous year.

The net operating profit amounted to EUR 240 million (EUR 194 million). Unrealised fair value changes amounted to EUR 27 million (EUR -3 million) in the financial year.

Changes to the regulation of banks’ capital adequacy (CRR II and CRD V) were applied at the end of June 2021. The Group’s leverage ratio was 12.8% (3.9%) at the end of December. MuniFin fulfils the CRR II definition of a public development credit institution and may therefore deduct all credit receivables from the central government and municipalities in the calculation of its leverage ratio. This change explains the growth of leverage ratio.

At the end of December 2021, the Group’s CET1 capital ratio remained very strong, 95.0% (104.3%). Tier 1 and total capital ratio were 118.4% (132.7%). The new CRR II regulation lowered the capital ratio mainly due to the changes in the calculation of the counterparty credit risk and CVA VaR. CET1 capital ratio nevertheless exceeded the total requirement of 13.4% by over seven times, with capital buffers accounted for.

The COVID-19 pandemic that broke out in March 2020 has now lasted almost two years, although its intensity has varied. As a whole, the pandemic has only had a minor effect on the Group’s financial standing. In this financial year, the demand for financing in the municipal sector remained lower than expected due to surprisingly good economic development and the Government’s temporary COVID-19 recovery measures in 2020.

Long-term customer financing, including both long-term loans and leased assets totalled EUR 29,214 million (EUR 28,022 million) and grew by 4.3% (13.0%) at the end of December. The total of new lending in January–December amounted to EUR 3,275 million (EUR 4,764 million). Short-term customer financing decreased by 16.9% (previous year’s growth was 62.9%) and reached EUR 1,089 million (EUR 1,310 million).

Of all long-term customer financing, the amount of green finance aimed at environmentally sustainable investments totalled EUR 2,328 million (EUR 1,786 million) and the amount of social finance aimed at investments promoting equality and communality totalled EUR 1,164 million (EUR 589 million) at the end of December. Green and social finance have been well received by customers, and the amount of this finance increased by 47.0% (88.0%) from the previous year.

In 2021, new long-term funding reached EUR 9,395 million (EUR 10,966 million). At the end of December, the total amount of acquired funding was EUR 40,712 million (EUR 38,139 million), of which long-term funding made up for EUR 36,893 million (EUR 34,243 million).

The Group’s liquidity has remained at a very good level. At the end of December, total liquidity amounted to EUR 12,222 million (EUR 10,089 million). The Liquidity Coverage Ratio (LCR) stood at 334.9% (264.4%) at the end of the year and the Net Stable Funding Ratio (NSFR) at 123.6% (116.4%).

The Board of Directors proposes to the Annual General Meeting to be held in spring 2022 a dividend of EUR 1.03 per share for 2021, totalling EUR 40,235,711.94. The total dividend payment for 2020 was EUR 20,313,174.96.

Outlook for 2022: The Group expects its net operating profit excluding unrealised fair value changes to be significantly lower than in the previous year, as per the Group’s long-term profitability targets and more beneficial customer pricing enabled by these targets. The Group expects its capital adequacy ratio and leverage ratio to remain very strong. The valuation principles set in IFRS 9 may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate in the short term.

Key figures (Group)

31 Dec 2021

31 Dec 2020

Net operating profit excluding unrealised fair value changes (EUR million)*

213

197

Net operating profit (EUR million)*

240

194

Net interest income (EUR million)*

280

254

New lending (EUR million)*

3,275

4,764

Long-term customer financing (EUR million)*

29,214

28,022

New long-term funding (EUR million)*

9,395

10,966

Balance sheet total (EUR million)

46,360

44,042

CET1 capital (EUR million)

1,408

1,277

Tier 1 capital (EUR million)

1,756

1,624

Total own funds (EUR million)

1,756

1,624

CET1 capital ratio, %**

95.0

104.3

Tier 1 capital ratio, %**

118.4

132.7

Total capital ratio, %**

118.4

132.7

Leverage ratio, %**

12.8

3.9

Return on equity (ROE), %*

10.7

9.4

Cost-to-income ratio*

0.2

0.2

Personnel

164

165

*Alternative performance measure. **Figures for the financial year 2021 are calculated in accordance with CRR II. Comparison periods have not been restated to reflect the updated capital requirements regulation.

Comment on the 2020 financial year by President and CEO Esa Kallio

Finland’s economic and employment situation exceeded expectations in 2021 and reached a surprisingly good level. The central government’s COVID-19 support package ensured that municipalities have not had to shoulder the negative economic effects of the pandemic.

Municipal sector’s demand for financing was lower than expected in 2021. The demand for state-subsidised housing finance grew moderately, as expected. MuniFin’s market position is strong, and we continue to be by far the largest single credit institution offering long-term loans for our customer base.

Despite the temporarily improved financial situation, the fiscal sustainability gap and structural problems in the public economy continue to exist. In 2022, we therefore expect the demand for financing in the municipal sector to return to the pre-pandemic level.

The European Union’s changes to the capital adequacy regulation were applied at the end of June. Under the new regulation, MuniFin gained the status of a public development credit institution, which significantly eases MuniFin’s ability to comply with the leverage ratio capital requirement. This has allowed us to increasingly transfer the benefit from negative interest rates to our customers, making our loan financing even more affordable than before. This change in our credit terms took force in October, and its benefits will begin to have a wider impact in the interest expenses of our loan customers in 2022.

Once again, our funding succeeded excellently, and the availability of funding in the international capital market remained good. Thanks to our effective funding, we were again able to ensure affordable financing for our customers.

The legislative package for Finland’s long-prepared health and social services reform was largely completed in June, allowing municipalities to launch practical preparations. In the future, MuniFin’s customers will include the new wellbeing services counties.

Our customers play a key role in mitigating climate change and promoting the green transition. We support our customers in this transition by offering them green finance and sharing our expertise. In 2021, the demand for our green finance continued to grow, and the social finance that we launched in 2020 established its position among our customers.

MuniFin’s year started with a renewed organisation and was characterised by renewal and the rooting of new operating models. I wish to thank our customers for their close collaboration and our staff for their excellent work during this year of external and internal upheaval.

Information on Group results

Consolidated income statement

01–12/2021

01–12/2020

Change, %

(EUR million)

Net interest income

280

254

10.3

Other income

4

2

85.4

Income excluding unrealised fair value changes

285

257

11.0

Commission expenses

-5

-5

-0.2

Personnel expenses

-18

-18

-0.3

Other items in administrative expenses

-17

-15

11.6

Depreciation and impairment on tangible and intangible assets

-16

-6

>100

Other operating expenses

-16

-15

6.6

Costs

-72

-58

22.4

Credit loss and impairments on financial assets

0

-1

-87.8

Net operating profit excluding unrealised fair value changes

213

197

8.0

Unrealised fair value changes

27

-3

<-100

Net operating profit

240

194

23.5

Profit for the financial year

192

155

23.4

The sum of individual results may differ from the displayed total due rounding. Changes of more than 100% are shown as >100% or <-100%.

Group’s net operating profit excluding unrealised fair value changes

MuniFin Group’s core business operations remained strong during 2021. The Group’s net operating profit excluding unrealised fair value changes grew by 8.0% (6.2%) and totalled EUR 213 million (EUR 197 million). Income excluding unrealised fair value changes was EUR 285 million (EUR 257 million) and grew by 11.0% (4.3%). The Group’s costs were EUR 72 million (EUR 58 million) rising by 22.4% from the previous year. The non-recurring item related to impairment on on-going IT system implementation, EUR 10.5 million, increased costs. Costs excluding the non-recurring item grew as predicted and were 4.4% higher than in previous year (-3.0%). The COVID-19 pandemic did not have a significant negative impact on the Group’s core business and profitability in 2021 or in comparison year.

Net interest income totalled EUR 280 million (EUR 254 million), and increased by 10.3% (5.8%) from the previous year. Net interest income was positively affected by growing volumes and low market interest rates. In October 2021, the Group changed the conditions of its long-term customer loans with variable interest rates so that its customers will benefit from negative reference rates better than before. This change only had a minor effect on the Group’s profits. The Group’s net interest income does not recognise the interest expenses of EUR 16 million of the AT1 capital instrument, as the capital loan is treated as an equity instrument in the consolidated accounts. The interest expenses of the capital loan are treated similarly to dividend distribution; that is, as a decrease in retained earnings under equity upon realisation of interest payment on an annual basis.

Other income grew from the previous year to EUR 4 million (EUR 2 million). Other income includes commission income, realised net income from securities and foreign exchange transactions, net income on financial assets at fair value through other comprehensive income, and other operating income. In addition, the turnover of MuniFin’s subsidiary company Financial Advisory Services Inspira is included in the other income.

During 2020, the COVID-19 pandemic slowed cost growth, making the year’s costs unusually low. Costs started rising again in 2021, although the growth was slower than before the pandemic.

Commission expenses totalled EUR 5 million (EUR 5 million) and consisted primarily of paid guarantee fees, custody fees and funding programme update fees.

Administrative expenses reached EUR 35 million (EUR 33 million) and grew by 5.2% (2.3%). Of this, personnel expenses comprised EUR 18 million (EUR 18 million) and other administrative expenses EUR 17 million (EUR 15 million). Personnel expenses were almost at the same level than in previous year and were 0.3% (0.8%) less than in 2020. There were no significant changes in employee numbers and the average number of employees in the Group was 162 (167). Salary and pension costs decreased slightly during the financial year.

Other items in administrative expenses grew by 11.6% (4.0%) during the financial year. The cost of maintaining and developing information systems has increased IT expenses, but on the other hand, the COVID-19 pandemic has reduced certain types of expenditure, such as travelling expenses both in 2021 and 2020. In 2019, MuniFin Group signed outsourcing agreements for IT end-user and infrastructure services as well as the operation of the business IT systems to improve operational reliability and the availability of services. This implementation project was completed in late 2021.

During the financial year, depreciation and impairment of tangible and intangible assets reached EUR 16 million (EUR 6 million). The item includes impairment of EUR 10.5 million on the Group’s significant on-going IT system implementation.

Other operating expenses increased by 6.6% (-17.1%) to EUR 16 million (EUR 15 million). Fees collected by authorities increased by 23.0% (13.6%) to EUR 9 million (EUR 7 million), mainly due to an increase in the contribution to the Single Resolution Fund, which grew by 30.5% to EUR 6.7 million (EUR 5.2 million). These fees excluded, other expenses were EUR 6 million (EUR 7 million), decreasing by 10.3% (-35.1%), mostly due to smaller purchases of external services compared to 2020. Other expenses include a provision of EUR 0.4 million related to a possible tax increase following a tax interpretation issue from previous years.

The amount of expected credit losses (ECL), calculated according to IFRS 9, decreased during the financial year and was EUR -0.1 million (EUR -0.9 million). MuniFin Group has updated the scenarios and weights used to calculate ECL.

In 2020, MuniFin Group recorded an additional discretionary provision (management overlay) of EUR 0.3 million to take into account the financial effects of the COVID-19 pandemic. This was due to the fact that the deteriorating financial situation of certain customer segments had not yet reflected in MuniFin Group’s internal risk ratings for these segments, and therefore the Group’s management decided to record an additional discretionary provision based on a group-specific assessment. The financial situation of these customer segments later improved, and the management decided to remove the additional discretionary provision in late 2021. At the end of 2021, the Group’s management decided to record an additional discretionary provision of EUR 0.4 million to take into account ECL model changes that will take place in 2022. During 2022, the Group will further develop loss given default (LGD) calculation of mortgage loans as well as lifetime ECL calculations.

The Group’s overall credit risk position has remained low. According to the management’s assessment, all receivables will be recovered in full and no final credit loss will therefore arise, because the receivables are from Finnish municipalities, or they are accompanied by a securing municipal guarantee or a state deficiency guarantee supplementing mortgage collateral. During the Group’s history of more than 30 years, it has never recognised any final credit losses in its customer financing.

At the end 2021, the Group had a total of EUR 19 (EUR 24 million) of guarantee receivables from public sector entities due to customer insolvency, which are still under 0.01% of total customer exposure. The credit risk of the liquidity portfolio has remained at a good level, its average credit rating being AA+ (AA+).

Group’s profit and unrealised fair value changes

The Group’s net operating profit was EUR 240 million (EUR 194 million). Unrealised fair value changes improved the Group’s net operating profit by EUR 27 million, while in the previous year it had a negative impact of EUR 3 million. In 2021, net income from hedge accounting amounted to EUR 5 million (EUR 4 million) and unrealised net income from securities transactions to EUR 22 million (EUR -7 million).

The Group’s effective tax rate during the financial year was 20.1% (20.0%). Taxes in the consolidated income statement amounted to EUR 48 million (EUR 39 million). After taxes, the Group’s profit for the financial year was EUR 192 million (EUR 155 million). The Group’s full-year return on equity (ROE) was 10.7% (9.4%). Excluding unrealised fair value changes, the ROE was 9.6% (9.6%).

The Group’s other comprehensive income includes unrealised fair value changes of EUR -3 million (EUR -32 million). During the financial year, the most significant item affecting the other comprehensive income was cost-of-hedging, EUR -3 million (EUR -16 million). The fair value change due to changes in own credit risk of financial liabilities designated at fair value through profit or loss totalled EUR 0.4 million (EUR -17 million).

On the whole, unrealised fair value changes net of deferred tax affected the Group’s equity by EUR 19 million (EUR -28 million) and CET1 capital net of deferred tax in capital adequacy by EUR 19 million (EUR -15 million). The cumulative effect of unrealised fair value changes on the Group’s own funds in capital adequacy calculations was EUR 31 million (EUR 12 million).

Unrealised fair value changes reflect the temporary impact of market conditions on the valuation levels of financial instruments at the reporting time. The value changes may vary significantly from one reporting period to another, causing volatility in profit, equity and own funds in capital adequacy calculations. The effect on individual contracts will be removed by the end of the contract period.

In accordance with its risk management principles, MuniFin Group uses derivatives to financially hedge against interest rate, exchange rate and other market and price risks. Cash flows under agreements are hedged, but due to the generally used valuation methods, changes in fair value differ between the financial instrument and the respective hedging derivative. Changes in the shape of the interest rate curve and credit risk spreads in different currencies affect the valuations, which cause the fair values of hedged assets and liabilities and hedging instruments to behave in different ways. In practice, the changes in valuations are not realised on a cash basis because the Group primarily holds financial instruments and their hedging derivatives almost always until the maturity date. Changes in credit risk spreads are not expected to be materialised as credit losses for the Group, because the Group’s liquidity reserve has been invested in instruments with low credit risk. In the financial year, unrealised fair value changes were influenced in particular by changes in interest rate expectations and credit risk spreads in the Group’s main funding markets.

Parent Company’s result

MuniFin’s total net interest income at year-end was EUR 264 million (EUR 238 million), and its net operating profit stood at EUR 223 million (EUR 178 million). The profit after appropriations and taxes was EUR 137 million (EUR 22 million). The interest expenses of EUR 16 million for 2021 on the AT1 capital loan, which forms part of Additional Tier 1 capital in capital adequacy calculation, have been deducted in full from the Parent Company’s net interest income (EUR 16 million). In the Parent Company, the AT1 capital loan has been recorded under the balance sheet item Subordinated liabilities.

Subsidiary Inspira

The turnover of MuniFin’s subsidiary company, Financial Advisory Services Inspira Ltd, was EUR 1.7 million for 2021 (EUR 2.8 million), and its net operating profit amounted to EUR 0.1 million (EUR 0.1 million).

Outlook for 2022

According to the MuniFin Group’s current view, global economic growth is slowing down, but the main trend in the economic outlook remains still relatively positive. Employment continues to have room for growth, household savings lend support to consumption potential and private investments are expected to remain at a good level. The first half of the year will suffer from the uncertainty caused by the coronavirus Omicron variant. The high price of energy and the ongoing component shortage will continue to cause cost pressures and take their toll on economic activity. Economic forecasts continue to be highly uncertain.

The main trends in monetary policy are the same in the United States and Europe, but their central banks will move at a considerably different pace. The risk of the economy overheating in the United States is real, and the central bank Fed is likely to have to raise its key interest rates several times, already in 2022. In the euro area, the increased inflation is still mainly explained by reasons that are expected to be temporary. The ECB’s new symmetrical inflation target of 2% leaves the central bank more leeway to ignore temporary cost-push inflation. The ECB is likely to scale down its non-standard measures in 2022, but presumably very gradually. It now seems that a prudent normalisation of the interest rate policy could begin in late 2023, when the euro area should reach its pre-pandemic growth path. The outlook in monetary policy continues to be highly prone to changes in the pandemic situation.

In Finland, labour shortage and the increasing price of necessities will slow down economic growth in 2022. GDP growth will nevertheless remain somewhat stronger than Finland’s long-term growth potential. Unemployment is expected to fall below 7%.

The central government’s COVID-19 support package will no longer boost municipal finances in 2022, returning the focus on structural imbalances. More specific assessments of how the health and social services reform will impact individual municipalities will not be available until spring 2022. The reform’s practical challenges and the uncertainty of its financial impact make it difficult to predict municipal finances over the next few years.

In 2022, the health and social services reform will be reflected in the Group’s operations as practical preparation to act as a financing counterparty to the new wellbeing services counties. It is difficult to estimate the wider economic impact of the reform at this stage, when there is no practical information available on how wellbeing services counties will function. Wellbeing services counties’ future level of investments will effect on MuniFin’s financing volumes, but on the other hand the operating expenditures of the counties will be covered from the government’s budget. In MuniFin’s financing operations, health and social services lending plays such a role that changes in it will not have a material impact on MuniFin’s financial development in the near future.

After confirmation of its status as a public development credit institution, MuniFin decided in June 2021 to change the conditions of its long-term customer loans with variable interest rates in a way that will allow customers to benefit from negative reference rates better than before, which will clearly make the Group’s 2022 net interest income lower than in the previous year. The Group’s customer operations and funding are expected to continue to run and develop steadily. Operating expenses are expected to grow from 2021, as investments in IT systems and operational reliability as well as the marked rise in supervisory fees all increase expenses.

Considering the above-mentioned circumstances, the Group expects its net operating profit excluding unrealised fair value changes to be significantly lower than in the previous year, as per the Group’s long-term profitability targets and more beneficial customer pricing enabled by these targets. The Group expects its capital adequacy ratio and leverage ratio to remain very strong. The valuation principles set in the IFRS regulatory framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate in the short term.

These estimates are based on a current assessment of the development of MuniFin Group’s operations and the operating environment.

Webinar for investors and other stakeholders

MuniFin Group’s results for the year 2021 will be presented to investors and other stakeholders in a results webinar held on 9 February 2022 at 2:00 pm EET. Register for the webinar here. Register here if you are not able to attend but wish to receive a recording.

Municipality Finance Plc

Further information:

Esa Kallio, President and CEO, tel. +358 50 337 7953

MuniFin (Municipality Finance Plc) is one of Finland’s largest credit institutions. The company is owned by Finnish municipalities, the public sector pension fund Keva and the Republic of Finland. MuniFin Group also includes the subsidiary company, Financial Advisory Services Inspira Ltd. The Group’s balance sheet is over EUR 46 billion.

MuniFin builds a better and more sustainable future with its customers. MuniFin’s customers are Finnish municipalities, municipal federations, municipally controlled entities and non-profit housing organisations. Lending is used for environmentally and socially responsible investment targets such as public transportation, hospitals and healthcare centres, schools and day care centres, and homes for people with special needs.

MuniFin’s customers are domestic but the company operates in a completely global business environment. The company is an active Finnish bond issuer in international capital markets and the first Finnish green and social bond issuer. The funding is exclusively guaranteed by the Municipal Guarantee Board.

Lari Toppinen is one of four people working with funding in MuniFin. His tasks include issuing benchmarks, private placements, hedging and, dealer and investor relations. During his first weeks he has been involved with several transactions, as the team has already reached 30% of this year’s EUR 9–10 billion long-term funding target.

– I would say it has been an exciting start to the year and I quite enjoy the fast-paced environment. Everyone in the team is extremely professional and helpful and I am impressed how fast our team can adapt to new situations and market conditions. I look forward to collaborating more in the coming months, Toppinen says.

– Lari is a team player with good analytical skills, which are key factors in succeeding in this position. He is a great addition to the team and we all look forward to working together, says Antti Kontio, Head of Funding and Sustainability.

Before joining MuniFin, Toppinen gained experience from capital markets at Danske Bank. Currently, he is finishing his master’s degree at Hanken School of Economics.

Toppinen applied to MuniFin as he was intrigued by the company’s reputation as Finland’s most active bond issuer and pioneer status on sustainable finance. Being able to work in a global business environment is also a huge motivational factor for him.

– I always knew I wanted to work in an international role. I completed my bachelor’s degree at Stockholm University and before that I spent six months in Canada studying sustainable investing. I also studied for a year in Spain when I was younger. I hope the situation will soon allow us to travel and meet our dealer banks and investors in person, Toppinen says.

In his free time, he enjoys a variety of sports such as cross-country and downhill skiing, and golf. He likes to spend time with his friends and family and is a big fan of stand-up comedy.

– Ricky Gervais is probably the world’s greatest comedian. His character in The Office is one of my all-time favourites. A fun fact about me is that I enjoy performing and acting myself whenever there is a chance, Toppinen smiles.

Lari Toppinen

Funding Analyst at MuniFin since 10 January 2022

Soon graduating from Hanken School of Economics, majoring in finance

Lives in central Helsinki

Hobbies include cross-country and downhill skiing, and golf

Enjoys stand-up comedy, acting and hanging out with friends and family

Joakim Holmström, Executive Vice President, Capital Markets & Sustainability

There will be a Q&A session after the presentations.

MuniFin’s results webinar

Time: 9 February 2022 2:00 pm (EET)

Registration: Please register for the webinar here.

The event is organized via Microsoft Teams.

A link to join the event will be sent to the registered e-mail. The webinar will be recorded and the recording will be sent to everyone who have registered.

Register here if you are not able to attend but wish to receive the recording.

MuniFin (Municipality Finance Plc) is one of Finland’s largest credit institutions: the Group’s balance sheet totals close to EUR 46 billion. The company is owned by Finnish municipalities, the public sector pension fund Keva and the Republic of Finland.

MuniFin builds a better and more sustainable future with its customers. MuniFin’s customers are Finnish municipalities, municipal federations, municipally controlled entities and non-profit housing organisations. Lending is used for environmentally and socially responsible investment targets such as public transportation, hospitals and healthcare centres, schools and day care centres, and homes for people with special needs.

MuniFin’s customers are domestic but the company operates in a completely global business environment. It is an active Finnish bond issuer in international capital markets and the first Finnish green and social bond issuer. The funding is exclusively guaranteed by the Municipal Guarantee Board.

The Municipality Finance Group also includes the subsidiary company, Financial Advisory Services Inspira Ltd.